Starting a pension in an entry level job in Ireland and knowing how to maximise pension growth are two sides of the same coin. The earlier you start a pension, the better, and it’s a great way to maximise pension growth.

You can start a pension at any stage of your career, but starting a pension in an entry level job is the best way to build a pension pot and ensure you maximise pension growth for retirement.

Advice on starting a pension and building it is invaluable at every stage of your career. Getting impartial advice is crucial, but the only way to ensure you are planning properly for the future.

National Pension Helpline can give that advice and get you started on building your pension.

Table of Content

What options are available to those entering the workforce?

There are many pension options open to those entering the workforce in Ireland. You will have a lot going on when starting your first job after college, but putting money away for the future is easy to do and will always be a benefit.

When taking up an entry level job, you may think retirement is years away and something you do not need to think about. The truth is that it is never too early to start planning for the future, and starting your pension is an excellent way to prepare for retirement, even if it is 40 years away.

Common pension options for those entering the workforce:

{kind=link}

{kind=link}

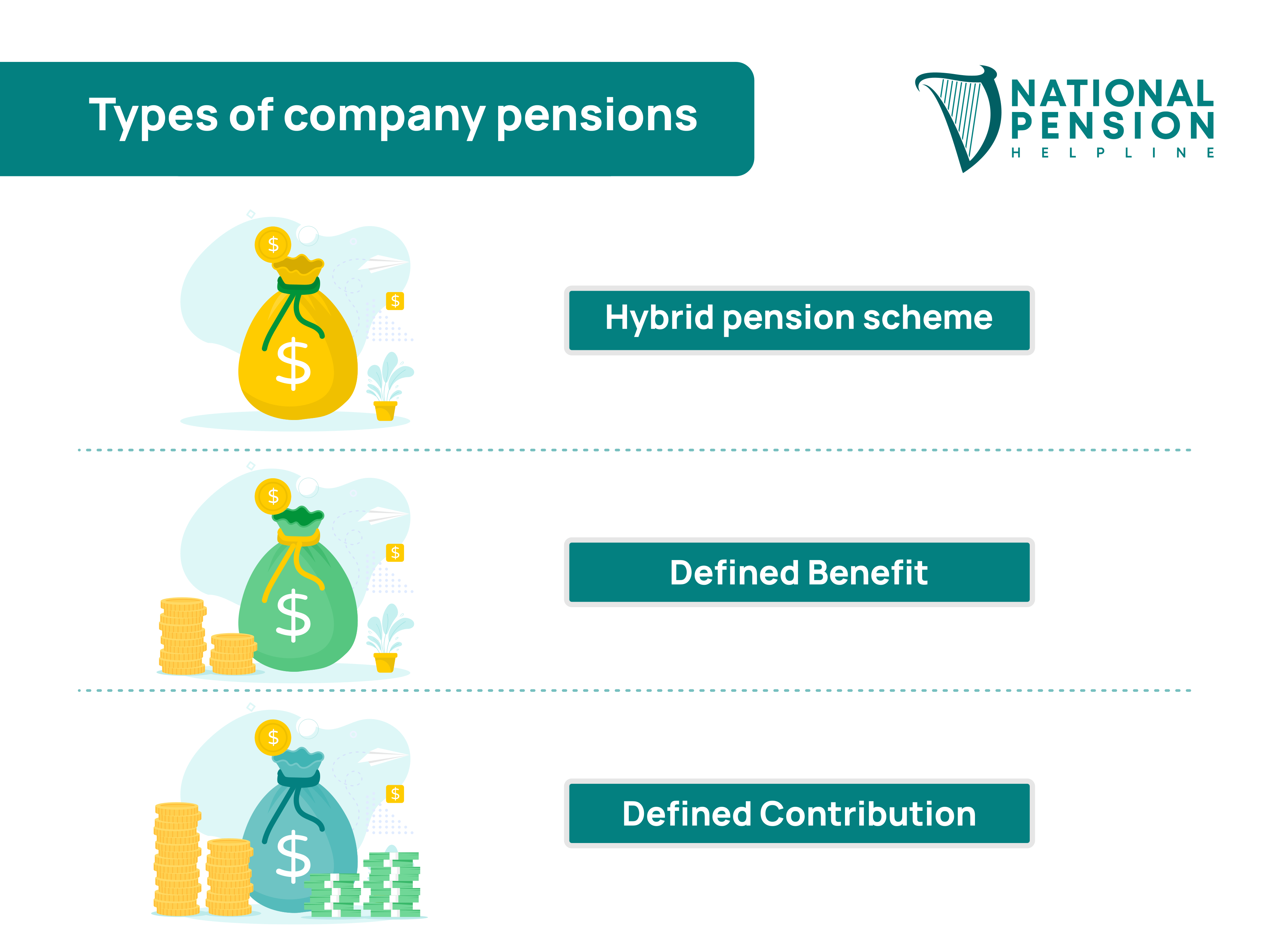

The company pension

The company pension can be a good starter option for those entering the workforce. You will need to do very little, and your company will make all the necessary deductions.

You can even take your pension contributions with you when you leave.

A drawback of the company pension is that it may not give you a great return on your investment. Pension growth could be slow, and you may even lose value due to inflation.

Personal Retirement Savings Account (PRSA)

A Personal Retirement Savings Account, PRSA, is a savings account that allows you to save for your retirement. You invest the money in various schemes, and the more you save, the more you can invest.

A PRSA is an excellent way to start your pension journey. You can tailor a plan to suit your needs, adjust it when you start earning more money, and you can take the PRSA with you when you change jobs.

The PRSA is flexible and can be the perfect way to start a pension in an entry level job and also maximise growth for when you retire.

The private pension scheme

The private pension scheme is one you can open as soon as you start work and with advice from an investment expert.

You can deduct payments from your monthly salary into the private pension scheme and keep it active when you move jobs or even take time off work.

A private pension scheme may not be a top priority when starting an entry level job, and you should only open one under trusted advice from a reliable source.

The State pension

The State pension is one you receive on reaching retirement age at 66. You qualify for the State pension when you make enough PRSI contributions during your working life.

Currently, you qualify for the State pension when you turn 66. If you make enough contributions, you qualify automatically, and the pension is not means-tested. The current weekly payment is €277.30.

The State pension payment amount is fixed, but there is not any growth, and it is not a great option if you have big retirement plans.

Hope for the best

The hope for the best option is not a very good one. Hoping to win the Lotto or starting a business that you can sell for millions is not a great way to plan for retirement, regardless of age.

You can contribute to a pension during your working life, invest in that pension pot and help it grow over the years and retire with a comfortable lifestyle when you reach pension age.

Congratulations if you win the Lotto in the meantime, but you will still have that nice pension to draw down when the time comes.

When you are young, you are in a better position to take risks with your choice of pension fund. You can decide how much to contribute, where to put the money and plan properly for retirement, even if you are only in your 20s.

How much can you contribute to your pension in your 20s?

You can contribute up to a maximum of 15% of your salary to your pension when you are aged under 30. The contributions are tax-free, and you can contribute up to 15% of your salary to any approved pension scheme to avail of the tax relief.

If you are over 30 years of age, you can contribute up to 20% of your salary to an approved pension scheme and get the tax relief on your contributions.

The tax relief is paid at the marginal rate of tax, the highest tax rate at which you pay tax. Most companies can deduct the pension contributions for you and handle the tax relief arrangements, too.

You can, of course, pay more money into your pension plan, but you will not get the tax relief when you exceed the threshold.

When starting an entry level job, the idea of pensions, pension contributions, max contribution amounts, and tax relief can be very daunting.

A qualified financial adviser will handle all your questions and get you started on the right plan and one to maximise pension growth. What is important is having the right pension to give you a comfortable retirement and one without financial worries.

How much do I need going into retirement in Ireland?

You need a large pension pot when going into retirement in Ireland. If you take early retirement or retire at the State pension age, 66, you could easily have 30 to 35 years ahead of you to fund, and it’s not cheap to live in Ireland.

According to the CSO, you need to take home around €15,000 per annum to avoid slipping into poverty, and that’s at today’s income and cost levels. The €15,000 does not include holidays, eating out, changing the car, home repairs and other extras; it only covers basic costs of living.

You would need a pension pot of €500,000 to give you enough of an annual pension of €16,000, a little more than the minimum you need to avoid slipping into poverty when you retire.

If you are starting off in your working life, you will need to look to the future and see how much you will need in 40 years to give you a comfortable retirement.

You will need more than the €500,000 pot to get by, and that is why you need to start a pension now to maximise your pension growth over the years of your working life.

What age can you access your pension in Ireland?

You can access your private pension in Ireland when you turn 50 years of age. It does not mean you can retire at 50, only that you can draw down a lump sum from the pension plan.

When you turn 50, you can draw down a maximum of 25% of your pension pot, tax-free. The maximum amount you may draw down is €200,000. If you wish to take a further lump sum, you will pay 20% tax on the amount you draw down.

With an occupational pension, you can only access the pot at 50 and if you no longer work for that company. If you still work for that company, you cannot access the pension pot for a lump sum until you turn 60.

You cannot access the State pension until you turn 66.

Early retirement is a dream of most people. The dream needs to be financed, and you can only afford to take early retirement if you have planned properly for your future.

An excellent way to plan for the future is to start a pension as soon as you get an entry-level job and invest in a plan to maximise pension growth.

How to start a pension

You can start a pension by filling out our free online assessment tool to speak with a Qualified Financial Advisor.

It is never too early to start a pension, and our Qualified Financial Advisors will advise you on the best pension options for entry level employees available today.

Anyone from the newly employed to the self-employed to business owners and executives looking at their retirement options should talk to one of our pension advisors.

Our assessment tool is easy to complete and is the best way to get an idea of your pension needs and how to get started on the best pension for you.

For the best pension advice and help getting started with a pension, please fill out our online assessment tool today.